Third-party processing built for Non-QM brokers.

Flat-fee mortgage processing designed to move files cleanly from submission through post-close.

Built by a broker who understands where Non-QM files actually break, how wholesale lenders operate, and what brokers need from a processor.

Reliable file management without in-house staff.

We provide third-party mortgage processing for brokers who need file ownership from disclosures through closing. The broker stays focused on origination; we keep the file moving.

Disclosures to closing

Our processor handles document collection, third-party orders, underwriting submission, condition management, closing coordination, and post-close updates.

Built for Non-QM realities

DSCR, bank statement, P&L, asset depletion, investor, and business purpose loans — files that need a processor who understands guidelines and exceptions.

Originate more, follow up less

For brokers who want operational leverage without hiring in-house staff. We hold the file. You hold the borrower relationship and the pipeline.

Non-QM files break in places retail processors don't see.

Most processing services are too retail-focused, too slow, or not built for Non-QM. This company exists to give brokers a processing partner who actually understands the files they are submitting.

Most processing is built retail-first.

Workflows assume W-2 borrowers, conventional documentation, and a single agency overlay. Non-QM does not fit.

Non-QM requires guideline literacy.

DSCR coverage tests, bank-statement income calcs, entity vesting, business-purpose structures, and lender-specific overlays — the file is the math.

Wholesale operates differently.

Conditions, redisclosures, and AE coordination move on a cadence that retail processors are not built for. We are.

Brokers needed a partner, not a vendor.

We were built broker-to-broker. The positioning is execution. The deliverable is a clean file.

What the processor handles, line by line.

One processor on the file from disclosures through post-close. No handoffs, no missing context, no chasing the lender's AE for status.

Simple, flat-fee pricing.

No percentage-based pricing. No margin compression. Predictable per-file processing costs you can quote against.

Full File Processing

- Initial disclosures to close

- Submission package preparation

- Third-party order coordination

- Underwriting submission

- Condition management

- Closing support

- Post-close updates

Streamlines & IRRRLs

- Streamline file support

- Document collection

- Submission coordination

- Condition tracking

- Closing support

- Post-close updates

We operate natively in Arive.

We keep the file updated from submission through post-close — milestones, conditions, notes, and status reflect what is actually happening in the file at any given moment.

- Arive file updates through the full loan cycle

- Milestone and condition tracking

- Notes and status updates maintained in the LOS

- Post-close updates completed

- Open to obtaining access to other LOS platforms used by broker partners

Open to working inside LendingPad, Byte, or other LOS platforms if access is provided by the broker.

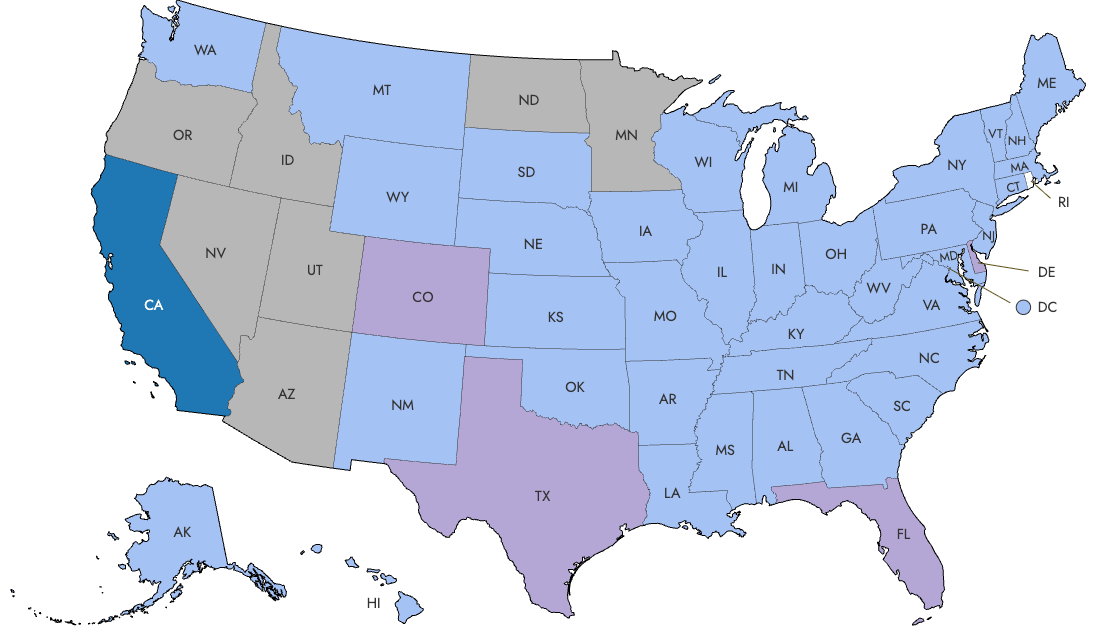

Coverage across the country.

California is fully licensed. Texas, Colorado, and Florida have licenses pending. The rest of the country runs business purpose loans only, in states where no broker license is required. Seven states are excluded until we're licensed there.

Built for brokers who need execution.

We are direct about who this works for — and who it doesn't. Both sides save time when expectations are aligned before a file is opened.

This is for you if —

You originate the loan; we run the file.

- Non-QM brokers

- DSCR-focused brokers

- Business purpose lenders and originators

- Brokers who need clean file management

- Brokers who do not want to hire in-house processing staff

- Small broker shops that need leverage

- High-volume LOs who need operational support

This is not the right fit if —

We won't pretend otherwise. Better for both of us upfront.

- Incomplete or disorganized intake

- Borrowers expecting retail hand-holding

- LOs who need origination training

- Files where the broker expects the processor to structure the deal, price the loan, or perform licensed origination activity

Five steps. One processor on the file.

Same processor, end to end. No handoffs between intake, submission, and closing teams. The file you submit is the file we close.

Submit the file

Broker provides the application, borrower docs, loan scenario, and lender direction.

We intake & organize

Processor reviews the file, identifies missing items, and prepares the submission package.

We submit & track

File is submitted to underwriting and tracked through conditions.

We coordinate closing

Processor works through final conditions, closing items, and lender requirements.

We update through post-close

File remains updated in the LOS through post-closing and audit items.

Need processing that understands Non-QM?

Send the file. We will run the process.